Tax Planning for the Years That Matter Most

Helping you reduce lifetime taxes through Roth conversion, withdrawal strategy, and timing decisions before and during retirement

Turn “I hope we’re not overpaying the IRS” into a clear, multi‑year tax strategy that supports your retirement income plan.

If you’re 5–10 years from retirement, taxes are no longer just an annual chore, they’re one of the biggest levers you have to extend the life of your savings. We help pre‑retirees design tax‑smart strategies around withdrawals, Roth conversions, and investment decisions, so more of your money funds your life instead of unnecessary taxes. Many people don’t realize that their withdrawal strategy directly affects their tax outcome in retirement →

This Isn’t About a Cleaner April Return

It’s about using the last 5–10 working years to set up a more flexible, tax‑efficient retirement.

Who we help:

— Pre‑retirees who expect to retire in roughly 5–10 years and want to be intentional about their tax picture.

— Busy professionals with high incomes, bonuses, or equity comp and multiple account types (401(k), IRA, Roth, brokerage).

— Couples who worry about future tax brackets, RMDs, and what happens “if one of us lives much longer than the other.”

If you’ve ever thought, “We might be fine, but I don’t want surprise tax bills later,” you’re in the right place. See how this fits into a broader retirement income plan.

The Moves Worth Making Before the Window Closes

Tax planning in the years before retirement covers more ground than most people expect. Here’s what we work through together:

-

The years between now and RMDs are often your best window to shift money into tax-free accounts at favorable rates. We model the right amount to convert, in the right years, to reduce your lifetime tax burden without triggering unintended consequences. Conversions done before you claim Social Security or hit RMD age are taxed at your lowest lifetime rate. That window narrows every year you wait. Visit our Roth Conversion Planning Guide to learn more.

-

We map your projected income across every year of retirement and identify where there’s room to deliberately fill lower brackets — through conversions, capital gains harvesting, or strategic withdrawals — before higher-income years force your hand.

-

In taxable accounts, we systematically capture losses to offset gains — reducing your current tax bill while keeping your portfolio on track. This isn’t a year-end scramble; it’s an ongoing strategy.

-

Your Medicare Part B and D premiums are directly tied to your income two years prior. A single year of high income from a Roth conversion, a home sale, or an RMD can trigger surcharges that cost thousands. We plan around those thresholds deliberately. Visit our Complete IRMAA Planning Guide to learn more.

Your Medicare premium in 2028 is based on your 2026 income. Decisions made this year are what can still change that number.

-

Required Minimum Distributions can force significant taxable income starting at age 73 — whether you need the money or not. We work to reduce future RMD exposure through Roth conversions and withdrawal sequencing before the distributions become mandatory

-

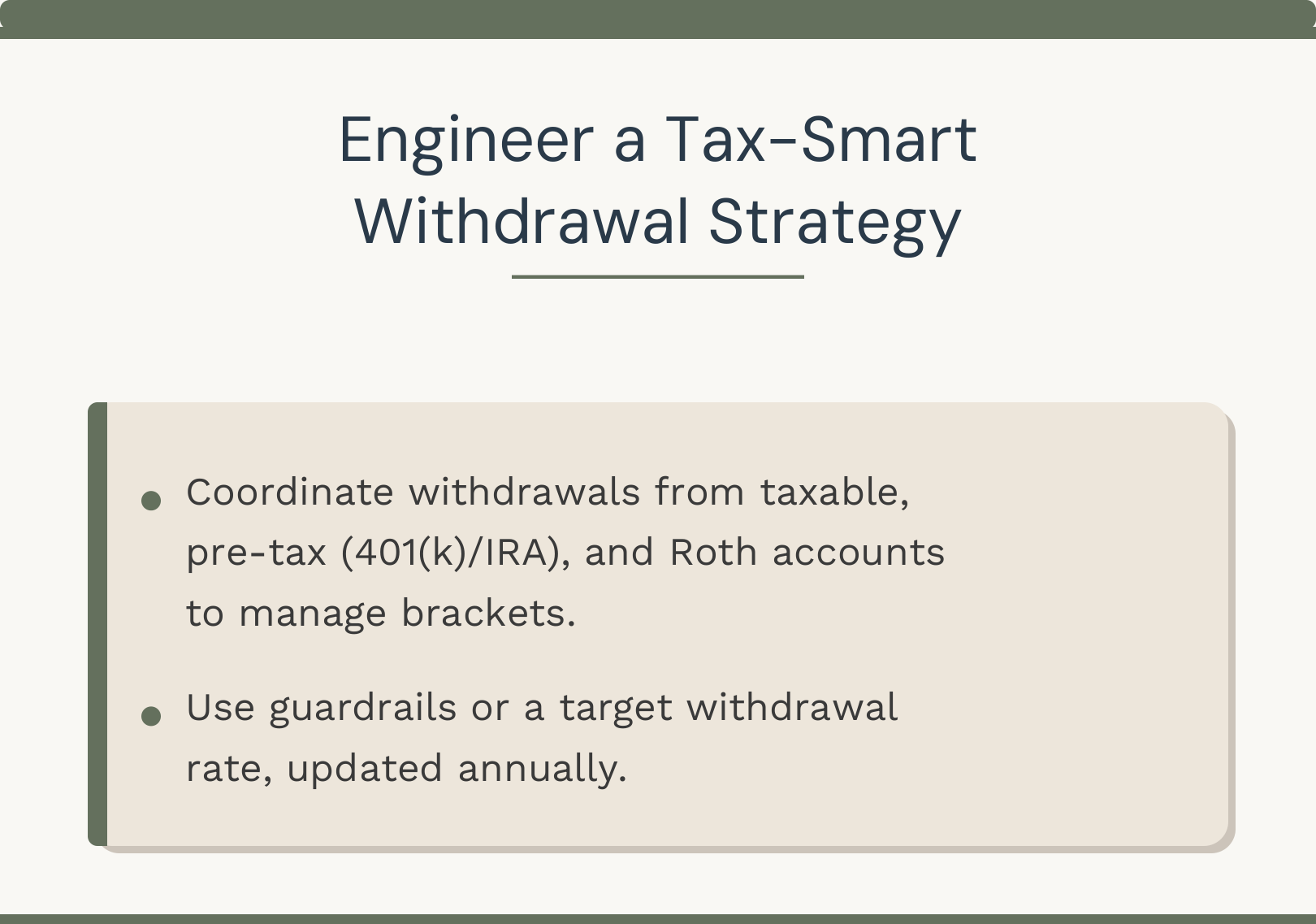

Which accounts you draw from — and in what order — has major tax implications over time. We build a multi-year withdrawal sequence that keeps your tax bracket in check and preserves flexibility as long as possible.

-

RSUs, stock options, and ESPP shares introduce concentrated risk and complex tax timing decisions. We help you manage vesting events, exercise timing, and diversification in a way that aligns with your broader retirement plan.

-

If you give to charity, there are tax-efficient ways to do it — including Qualified Charitable Distributions from your IRA after age 70½ that satisfy RMDs without the tax hit. We build giving into the plan rather than treating it as an afterthought.

-

When one spouse passes, the surviving spouse often faces a sudden jump from married filing jointly to single tax rates — on the same income. We plan for that transition proactively, often years in advance, so it doesn’t become a financial shock on top of a personal one.

Free Guide: 10 Tax Strategies for High-Income Pre-Retirees

A practical overview of the moves worth making in the 5–10 years before you retire — before the planning window closes.

If you’re a high earner approaching retirement, several of these strategies have a time limit. This guide walks through the ones most likely to matter for your situation.

We Don't Chase Loopholes. We Build a Plan

We don’t chase loopholes. We build a practical, written plan that connects your tax decisions to your retirement income strategy.

Map Your Lifetime Tax Picture

We start by projecting your income — from every source — across every year of retirement. Social Security, RMDs, withdrawals, pensions, investment income. Most people have never seen this picture. It changes everything about how you plan.

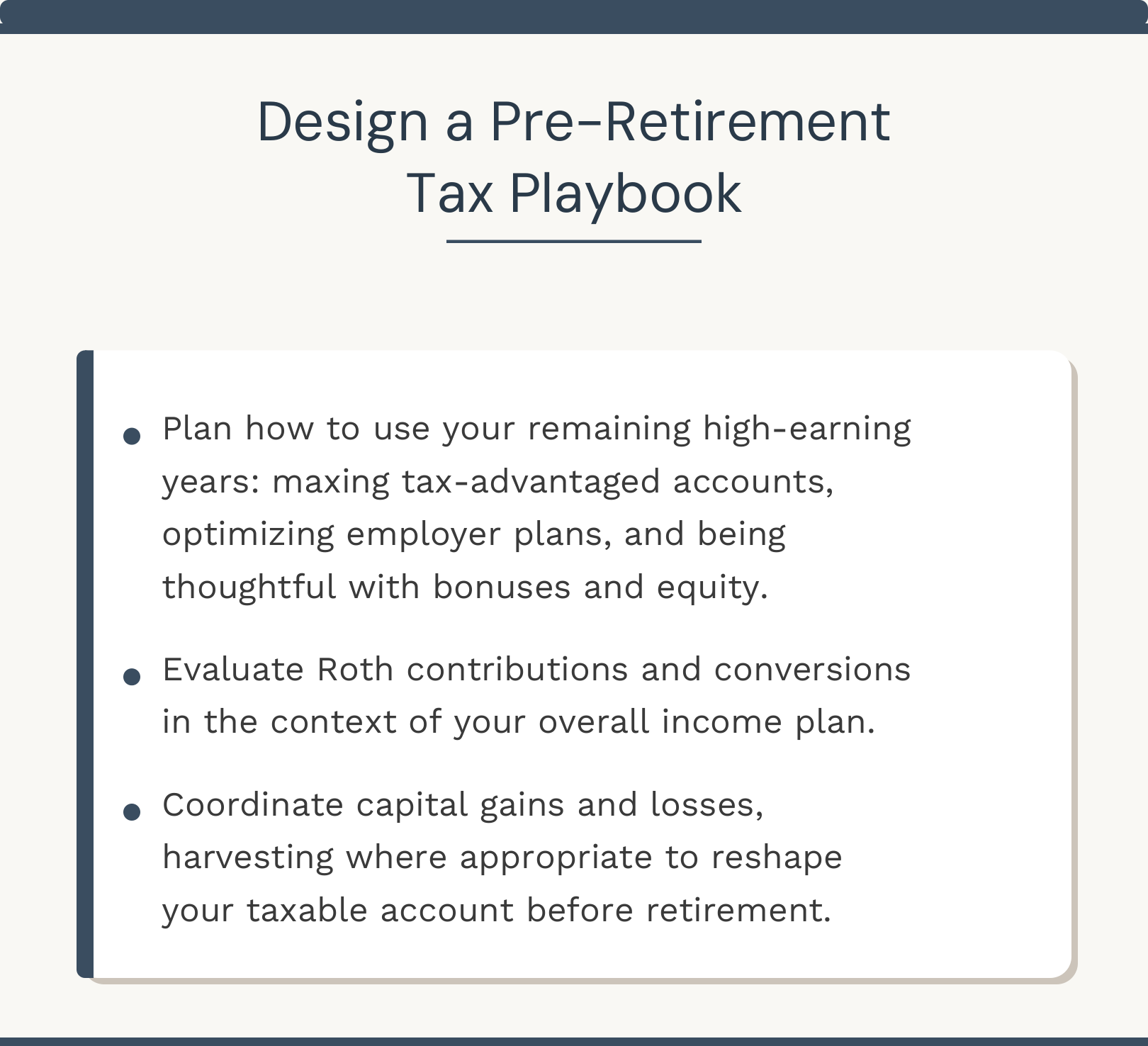

Design a Pre-Retirement Tax Playbook

With the full picture in view, we identify the specific moves worth making before you retire — Roth conversion windows, bracket-filling opportunities, equity comp decisions, charitable strategies — and sequence them into a written, year-by-year plan.

Integrate Taxes With Your Retirement Income Plan

Tax decisions don’t happen in isolation. Every conversion, every withdrawal, every investment decision has income implications. We ensure your tax strategy and your retirement income plan are always working in the same direction.

Learn how we coordinate taxes, investments, and retirement income →.

Thoughtful strategy, applied consistently over time

“Patrick has been my financial advisor for over 15 years. His honesty, collaboration, communication, and strategic vision have consistently driven my portfolio to new heights.”

— Jeff S., Laguna Niguel, CA

Testimonials are provided by current clients. They are unpaid, may not be representative of all clients, and are not a guarantee of future performance or success.

Ready to Stop Guessing and Start Planning?

If you’re 5–10 years from retirement and want a proactive tax strategy built around your income plan — not just a cleaner April return — let’s spend 20 minutes together to see if we’re the right fit.

No pressure. No sales pitch. Just an honest conversation about what’s possible before the window closes.

Not ready to call yet?