Your Portfolio Has A New Job: Retirement Income

For professionals 5-10 years from retirement who want a clear, tax-efficient income plan

You’ve spent decades doing one thing with your money: building it.

But as retirement gets closer, the goal shifts.

It’s no longer about accumulation — it’s about turning what you’ve built into a reliable, tax-efficient paycheck that lasts the rest of your life.

Most people don’t realize how much changes in that transition…until they’re already in it.

Once RMDs start, you lose the ability to control when and how much income you recognize. Planning before that age gives you options you won’t have after.

In 20 minutes, we’ll identify your biggest retirement tax leak and map out what a real retirement paycheck could look like for you

“He always listens… is thoughtful and strategic… and I feel confident in his recommendations.”

— Elizabeth L

Testimonials are provided by current clients. They are unpaid, may not be representative of all clients, and are not a guarantee of future performance or success.

The 5 Years Before Retirement Are the Most Financially Consequential of Your Life

This is the phase where small decisions can have lasting consequences.

— When should you start Social Security?

— Which accounts should you draw from first?

— How do you manage taxes across IRA, Roth, and brokerage accounts?

— How much income can you safely generate without running out?

— How do you avoid Medicare premium surcharges (IRMAA) that quietly raise your costs for years?

Most portfolios are built for growth.

Very few are designed to produce reliable, tax-efficient income.

And that gap is where unnecessary risk shows up.

When Building Stops, a Different Plan Begins

Once retirement is within reach, financial planning stops being about accumulation and starts being about turning what you’ve built into income you can actually live on.

The focus shifts to:

— Building a retirement paycheck designed to last 25–30 years

— Sequencing withdrawals to keep your lifetime tax bill as low as possible

— Aligning your portfolio to fund your life — not just grow a number

— Adapting as tax laws, markets, and your life change

Everything works together. Not in isolation.

Here’s how we structure that transition.

Four Steps. One Direction

Step 1 - A 20-Minute Conversation to Find Your #1 Risk

A brief conversation to understand where you are and what you’re trying to solve.

Step 2 - We Build the Full Picture of Your Retirement Math

We organize everything — investments, taxes, income sources — and identify opportunities and gaps.

Step 3 - You Get a Clear, Tax-Efficient Retirement Paycheck Plan

You'll see how your income is generated, how taxes are managed, and how we keep you below the Medicare premium (IRMAA) thresholds that catch most retirees off guard.

Step 4 - We Adjust as Life and Tax Laws Change

Annual reviews, proactive tax planning, and a direct line when life changes so your income, taxes, and investments stay aligned year after year.

“Laser-focused on my personal ambitions and financial success… we set up a SEP plan that I now maximize every year… I’ve moved all my accounts to Sentient Financial—and I’m so glad I did.”

— Kathleen K.

Testimonials are provided by current clients. They are unpaid, may not be representative of all clients, and are not a guarantee of future performance or success.

Work Directly With Patrick

For over 18 years, I’ve helped people make the shift from building wealth to living off it.

I’m Patrick Thompson, Accredited Wealth Management Advisor™ and founder of Sentient Financial.

Most of my clients come to me 5 to 10 years before retirement, when the decisions you make carry the most weight. When to retire, how to draw from your accounts, how to reposition your investments to generate income, keep pace with inflation, and still grow over time, and how to manage taxes... these decisions can either support your plan or quietly work against it. That includes knowing how to avoid Medicare premium surcharges like IRMAA that catch most retirees off guard.

My job is to take what feels complicated and turn it into a clear, reliable monthly income plan. That includes decisions around 401(k)s, IRAs, Social Security timing, and the tax impact, all organized so you know exactly where you stand.

As a fee-only fiduciary, I work for you. No commissions, no product sales, and no divided loyalties.

Based in Laguna Niguel, I serve pre-retirees throughout South Orange County — Irvine, Newport Beach, San Clemente, and beyond — as well as clients across the country through virtual planning. If you're within 5–10 years of retirement and want a clear income and tax strategy, geography doesn't have to be a barrier.

Outside of work, I’m a husband of 25 years and a father of two. I spend my free time hiking, fishing, and occasionally embarrassing myself on a golf course. And I’ve been a Kansas City Chiefs fan since I was 13. Loyalty matters, on and off the field.

In 20 minutes, we’ll pinpoint your single biggest retirement tax or income risk and you’ll leave with a clear next step, whether we work together or not..

Preparing for Retirement?

If you’re within 5–10 years of retirement, this series shows how to turn your savings into a reliable, tax-efficient retirement paycheck. Each episode walks through the key decisions—from income and taxes to Social Security and investment strategy—so you can approach retirement with clarity and confidence.

Who This Planning is Designed For

This is typically a good fit if you:

— Are within 5-10 years of retirement

— Have $500K—$5M+ saved across retirement and brokerage accounts

— Want clarity on how to turn your savings into income

— Care about reducing taxes—not just this year, but over time

— Prefer a thoughtful, long-term approach over quick answers

Featured Article

Independent. Fee-Only. Fiduciary.

Sentient Financial is an independent, fee-only advisory firm serving pre-retirees in Laguna Niguel, South Orange County, and virtually across the United States.

That means:

— No commissions

— No proprietary products

— No outside incentives influencing recommendations

Just advice and planning designed around what’s in your best interest.

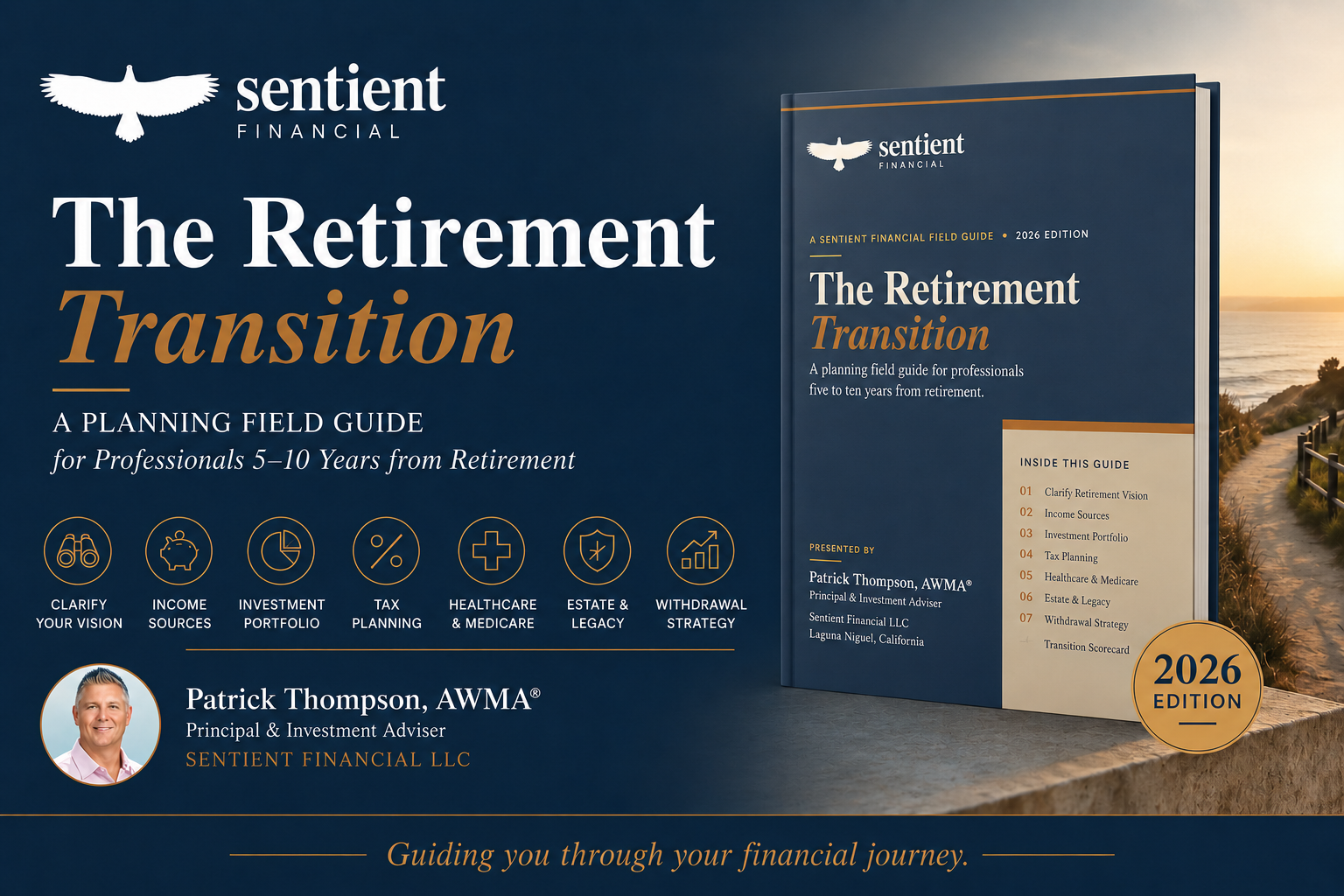

Find Out What Your Retirement Paycheck Could Actually Look Like Start Here.

Download the free Retirement Transition Field Guide — built for professionals 5–10 years from retirement who want clarity, not guesswork.

It’s a practical way to organize your thinking before making any major moves.

Every year you wait to fill lower brackets deliberately is a year of that room going unused, permanently.

The Best Time to Build Your Retirement Plan Is Now — Before the Window Closes

Many people wait too long because they feel like they should have everything figured out first.

You don’t.

You just need a starting point and a clear next step.

If you’re getting close to retirement and want to understand how all the pieces fit together, we can start with a simple conversation.

Some Clients Bring Their Kids

“Patrick has been our financial advisor over 10 years… he now works with our grown children, business clients, and closest friends… we recommend him highly.”

— Teresa C.

Testimonials are provided by current clients. They are unpaid, may not be representative of all clients, and are not a guarantee of future performance or success.

If you’re getting close to retirement and want to understand how this applies to your situation, that’s where our conversation starts.