What Is IRMAA? How High Earners Pay More for Medicare

What is IRMAA and how can it significantly affect your retirement income?

What Is IRMAA? How High Earners Pay More for Medicare

You worked hard, saved diligently, and built a retirement nest egg north of a million dollars. Then Medicare sends you a bill that's double what your neighbor pays — for the exact same coverage. That's IRMAA at work. For a married couple in the highest bracket, it can mean $13,872 in extra Medicare premiums every single year. It doesn't matter that you're on a fixed income now; the IRS reported your income two years ago, and Social Security is collecting on it today. Understanding what IRMAA is and how it's calculated is the first step toward doing something about it.

What Is IRMAA, in Plain English?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is a surcharge added on top of your standard Medicare Part B and Part D premiums when your income exceeds certain thresholds. In 2026, IRMAA kicks in for individuals earning more than $109,000 and for married couples earning more than $218,000 based on your tax return from two years prior.

How IRMAA Works: The Mechanics

Medicare is not a flat-fee program for everyone. The federal government means-tests Part B (medical insurance) and Part D (prescription drug coverage) premiums, meaning higher earners pay higher premiums. The Social Security Administration (SSA) determines your IRMAA status each fall by reviewing your most recently available tax return typically the return filed two years before the upcoming premium year.

Here is how the calculation flows:

1. SSA pulls your MAGI. Your Modified Adjusted Gross Income (MAGI) for IRMAA purposes is your Adjusted Gross Income (AGI) plus tax-exempt interest income. It does not include unrealized gains or money that never hits a tax return.

2. SSA matches your MAGI to a bracket. There are five surcharge tiers above the base premium. The higher your MAGI, the higher the surcharge.

3. SSA sends you a notice. In the fall before a new premium year, you will receive a letter called an Initial Determination telling you what you will pay.

4. The surcharge is deducted from your Social Security check. If you are receiving Social Security benefits, the premium (including any IRMAA) comes out automatically.

What Counts as Income for IRMAA?

MAGI for IRMAA purposes can surprise people. The following all count:

- Wages, salary, and self-employment income

- Traditional IRA and 401(k) withdrawals

- Required Minimum Distributions (RMDs)

- Capital gains (short-term and long-term)

- Rental income

- Pension distributions

- Tax-exempt municipal bond interest (this one catches people off guard)

- Social Security benefits that are included in your AGI

What does not count: Roth IRA withdrawals, health savings account (HSA) distributions, return of principal from non-qualified annuities, and life insurance proceeds.

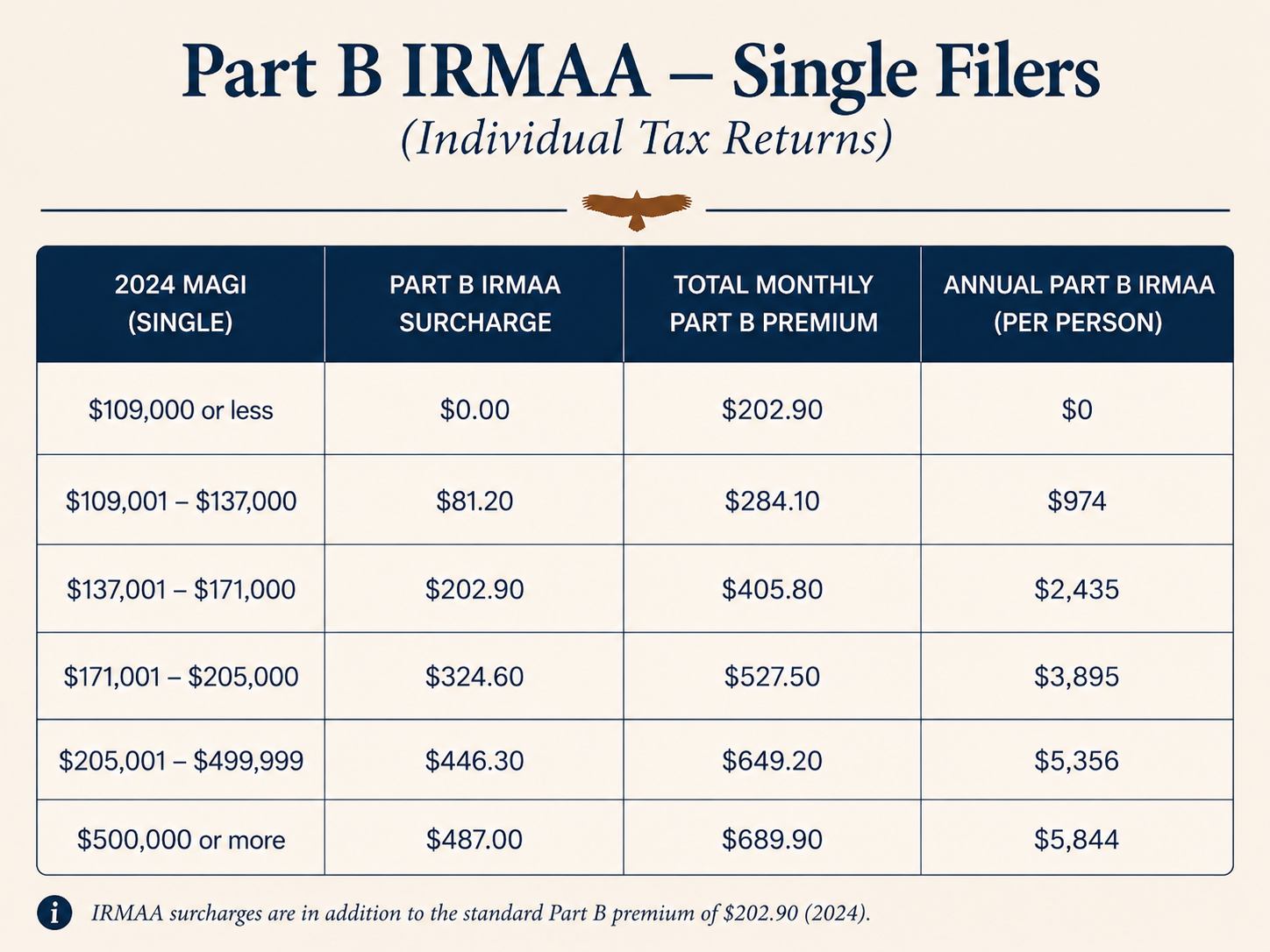

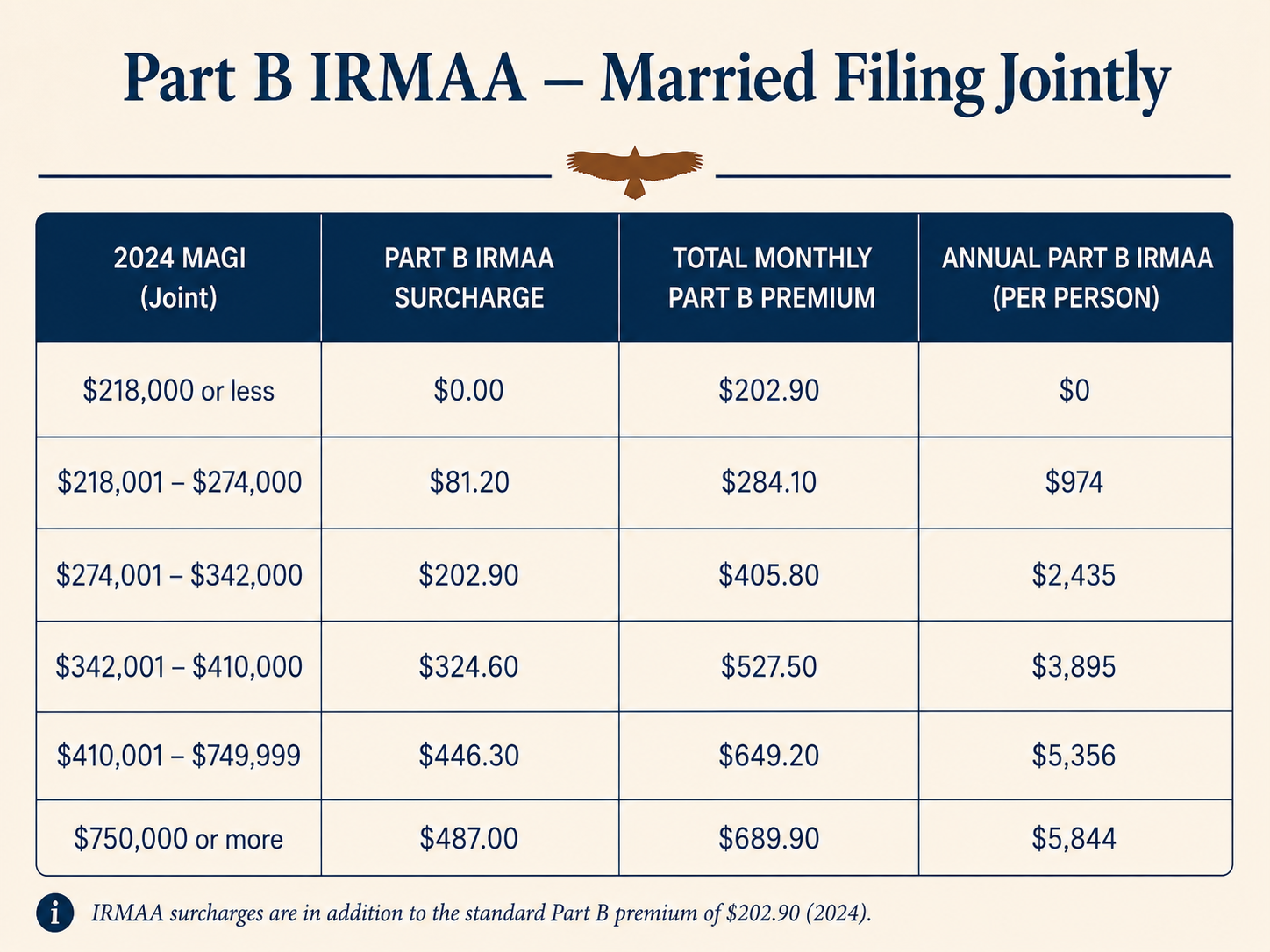

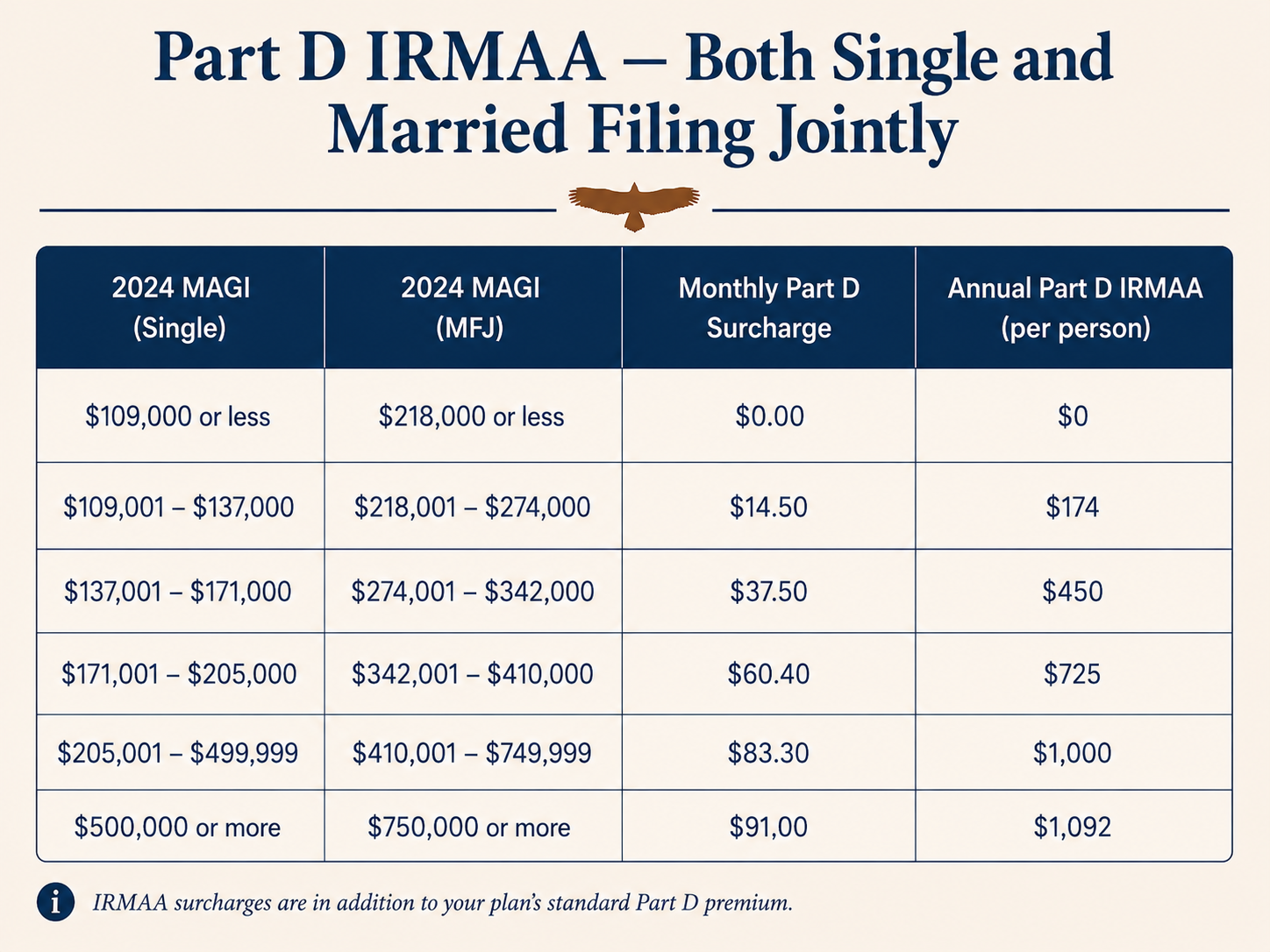

The 2026 IRMAA Surcharge Tiers

The 2026 IRMAA brackets (https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles) are based on your 2024 MAGI. Here is what the surcharges look like, per person, per month:

*Source: [Centers for Medicare & Medicaid Services, 2026 Medicare Parts A & B Premiums and Deductibles](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles)*

To put that in annual dollars: a single person in the first IRMAA bracket ($109,001–$137,000) pays an extra $1,148 per year in combined Part B and Part D surcharges. A couple in the fifth- bracket ($410,001–$749,999) pays an extra $12,712 per year — because each spouse is assessed separately — above what a non-IRMAA couple pays for the same Medicare coverage..

Why IRMAA Hits Pre-Retirees and New Retirees Especially Hard

IRMAA is not primarily a problem for people who have been retired for 15 years and are living off Social Security and a modest IRA. It is most punishing in the years immediately around retirement and here is why.

The Working-Year Income Problem

If you retire at 64 or 65, the income you earned at 62 or 63 while you were still in your peak earning years is what Social Security uses to set your initial Medicare premiums. A surgeon, senior executive, or successful business owner can easily have $400,000+ in MAGI in their last full working year. That translates directly into IRMAA surcharges the moment Medicare begins, even if your actual income in retirement is far lower

The Roth Conversion Trap

Roth conversions converting pre-tax IRA or 401(k) money into a Roth IRA are one of the most powerful retirement tax tools available. But they add directly to your MAGI in the year of conversion. A $100,000 Roth conversion that bumps a married couple from $265,000 in MAGI to $365,000 in MAGI does not just trigger income taxes. It pushes them from Tier 1 into Tier 3 IRMAA, costing them $975.60 per person, per month, in Medicare Part B premiums two years later. Careful conversion planning, specifically calibrated to IRMAA thresholds, is essential. Learn more about Roth conversion timing.

The RMD Problem

Required Minimum Distributions from traditional IRAs and 401(k)s begin at age 73. For someone with a $2 million IRA, the first year's RMD might be roughly $75,000. That income does not disappear, it stacks on top of Social Security, pension income, and any other distributions. High-balance IRAs can push retirees into IRMAA brackets year after year, with no easy way to escape unless they began Roth conversions before age 73.

Common Mistakes That Make IRMAA Worse

Many of the pre-retirees I work with are surprised to learn that some of their best-intentioned financial moves can worsen IRMAA exposure:

- Delaying Roth conversions until after RMDs begin. Once RMDs are required, you cannot stop them, and any Roth conversions on top of mandatory RMDs can push you into a higher IRMAA tier.

- Selling a business or investment property without IRMAA planning. A large capital gain in a single year can trigger IRMAA two years later and there is no way to unring that bell retroactively.

- Overlooking tax-exempt bond interest. Municipal bond interest does not appear in your taxable income, so many people forget it counts toward MAGI for IRMAA purposes.

- Taking large IRA distributions early in retirement "just in case." An ad-hoc $200,000 distribution to build up cash reserves can have Medicare premium consequences that last far longer than the cash does.

What You Can Do About IRMAA

There are four primary strategies for reducing or managing IRMAA exposure:

1. Plan Roth conversions within IRMAA bracket boundaries. Rather than converting as much as possible in a single year, work with an advisor to identify the precise MAGI level that keeps you in your current IRMAA tier and convert up to that amount.

2. Use Qualified Charitable Distributions (QCDs). If you are 70½ or older and charitably inclined, QCDs allow you to send up to $105,000 directly from your IRA to a charity. QCDs satisfy your RMD but do not count as income, meaning they do not raise your MAGI.

3. Harvest losses to offset gains. If you have taxable account investments with unrealized losses, harvesting those losses can offset capital gains and reduce MAGI.

4. Appeal using Form SSA-44 if you had a life-changing event. If your income dropped significantly due to retirement, divorce, death of a spouse, or other qualifying events, you can request that Social Security use a more recent year's income for IRMAA purposes.

The window for effective IRMAA planning typically runs from your early sixties until RMDs begin at 73. Planning during that window, not reacting to Medicare bills after the fact is where the real value is. See our full IRMAA planning guide.

Frequently Asked Questions About IRMAA

What does IRMAA stand for?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is the additional amount higher-income Medicare beneficiaries pay each month on top of the standard Part B and Part D premiums.

At what income does IRMAA kick in for 2026?

For 2026, IRMAA begins at a 2024 MAGI above $109,000 for individuals and above $218,000 for married couples filing jointly. If your income is at or below those thresholds, you pay the standard $202.90 Part B premium with no surcharge.

Does IRMAA apply to both Medicare Part B and Part D?

Yes. IRMAA surcharges apply to Medicare Part B (medical insurance) and to Medicare Part D (prescription drug coverage). The surcharge amounts differ for each part.

Can I get rid of IRMAA once it is assessed?

You can appeal an IRMAA determination if your income has dropped due to a qualifying life-changing event — retirement, divorce, death of a spouse, loss of income-producing property, or reduction in work hours. You file [Form SSA-44](https://www.ssa.gov/forms/ssa-44.pdf) with the Social Security Administration.

Does Roth IRA income affect IRMAA?

No. Qualified distributions from a Roth IRA are not counted in your MAGI for IRMAA purposes. This is one of the primary reasons Roth conversions done carefully and within the right income limits are a valuable IRMAA management tool for retirees.

My income is lower this year. Can IRMAA be adjusted?

Yes, but only if the reduction is due to a qualifying life-changing event, or if Social Security is using an older tax return (say, two years ago) when a more recent return shows lower income. You can request that Social Security use the more recent year by filing Form SSA-44.

Ready to See What IRMAA Could Cost You and What to Do About It?

If your household income has been above $200,000 in recent years, IRMAA is not a hypothetical, it is a line item in your retirement budget. The planning window to reduce it is finite, and every year of inaction is a year of missed opportunity. I offer a complimentary 20-minute Retirement Fit Call where we can take a quick look at your income trajectory, your current Medicare exposure, and whether there are steps worth taking in the next 12 months. There is no obligation and no sales pitch just a clear-eyed conversation about your situation.

Schedule your Retirement Fit Call here.

*Sentient Financial, LLC is a state-registered investment adviser in California. This information is for educational purposes only and does not constitute investment, tax, or legal advice. Nothing here should be taken as a recommendation to buy or sell securities or to implement a specific strategy. Past performance does not guarantee future results. IRMAA figures referenced are for the 2026 benefit year, based on 2024 MAGI, as published by the Centers for Medicare & Medicaid Services.*