The Complete Guide to IRMAA Planning for Pre-Retirees and Retirees (2026 Edition)

A married couple with $250,000 of MAGI in retirement pays $2,538 more for Medicare in 2026 than a couple earning $200,000 — the same coverage, the same doctors, the same drugs. Just a different spot on an income table most people have never seen.

That extra cost is IRMAA — the Income-Related Monthly Adjustment Amount — and for high-income retirees and pre-retirees, it is one of the most impactful and least understood pieces of the retirement income puzzle.

This guide is written for people aged 55 to 70 with $1 million or more in investable assets who are either approaching Medicare enrollment or already enrolled. If you have a pension, a large IRA, a taxable brokerage account, or income that varies significantly year to year, IRMAA planning deserves a dedicated place in your retirement income strategy.

Inside, you will find the full 2026 IRMAA bracket tables, a plain-language explanation of how surcharges are calculated, the eight most common triggers, seven strategies to minimize or avoid them, and a step-by-step guide to appealing an IRMAA determination if your income has recently dropped.

What Is IRMAA?

IRMAA — Income-Related Monthly Adjustment Amount — is a surcharge added to your standard Medicare Part B and Part D premiums if your income exceeds certain thresholds. It is not a penalty in the disciplinary sense; it is simply a means-tested pricing structure that causes higher-income beneficiaries to pay more for the same Medicare coverage everyone else receives.

The Social Security Administration (SSA) determines whether you owe IRMAA by reviewing your federal tax return from two years prior. That look-back period is built into federal law and cannot be waived except in specific life-changing circumstances.

IRMAA is not a flat fee. It is tiered across six income levels, and crossing even one dollar into a higher bracket triggers the full surcharge for that tier — for the entire year. Calculator: Will IRMAA Cost Me Money?

How IRMAA Fits into Medicare Part B and Part D Premiums

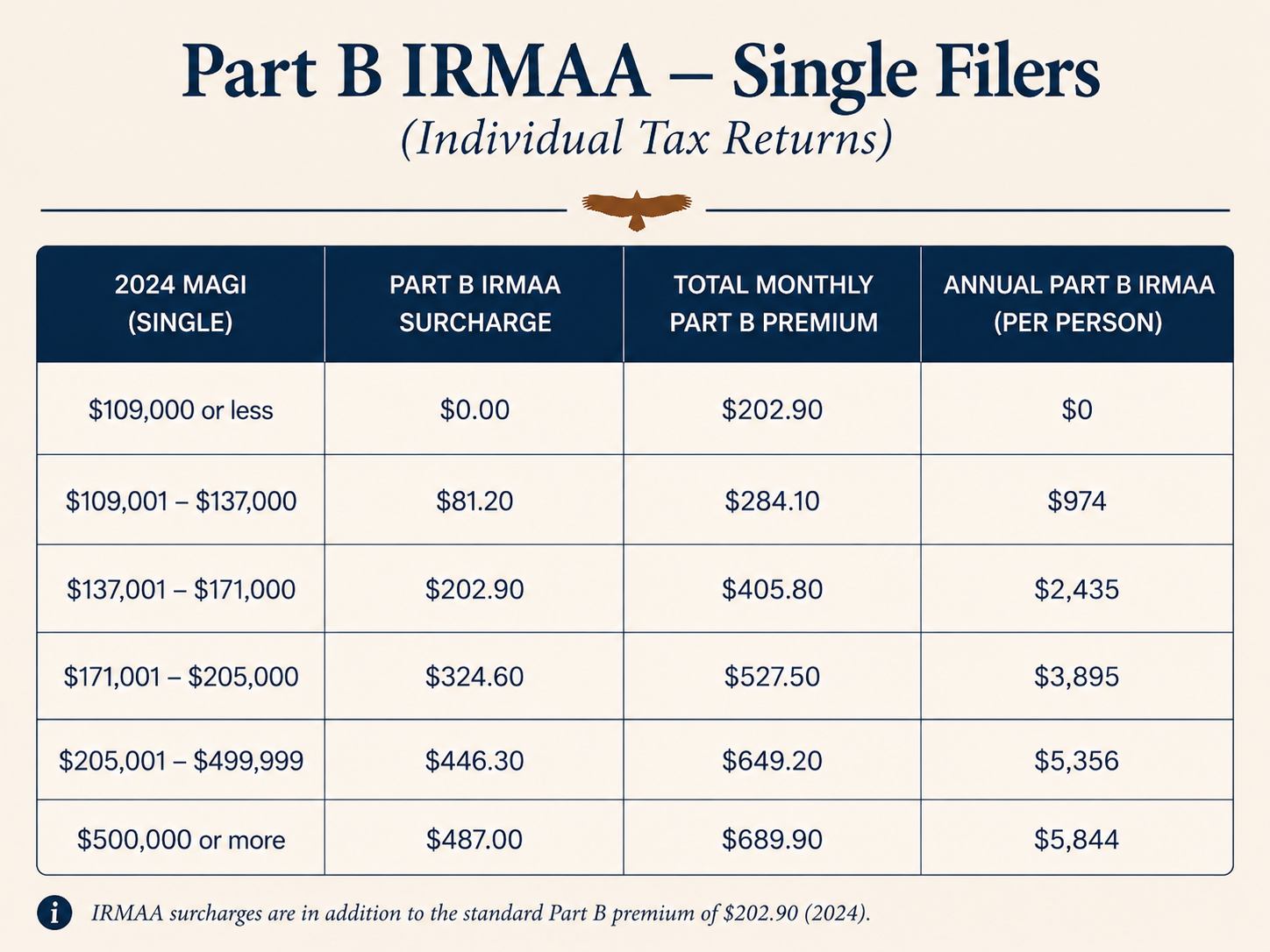

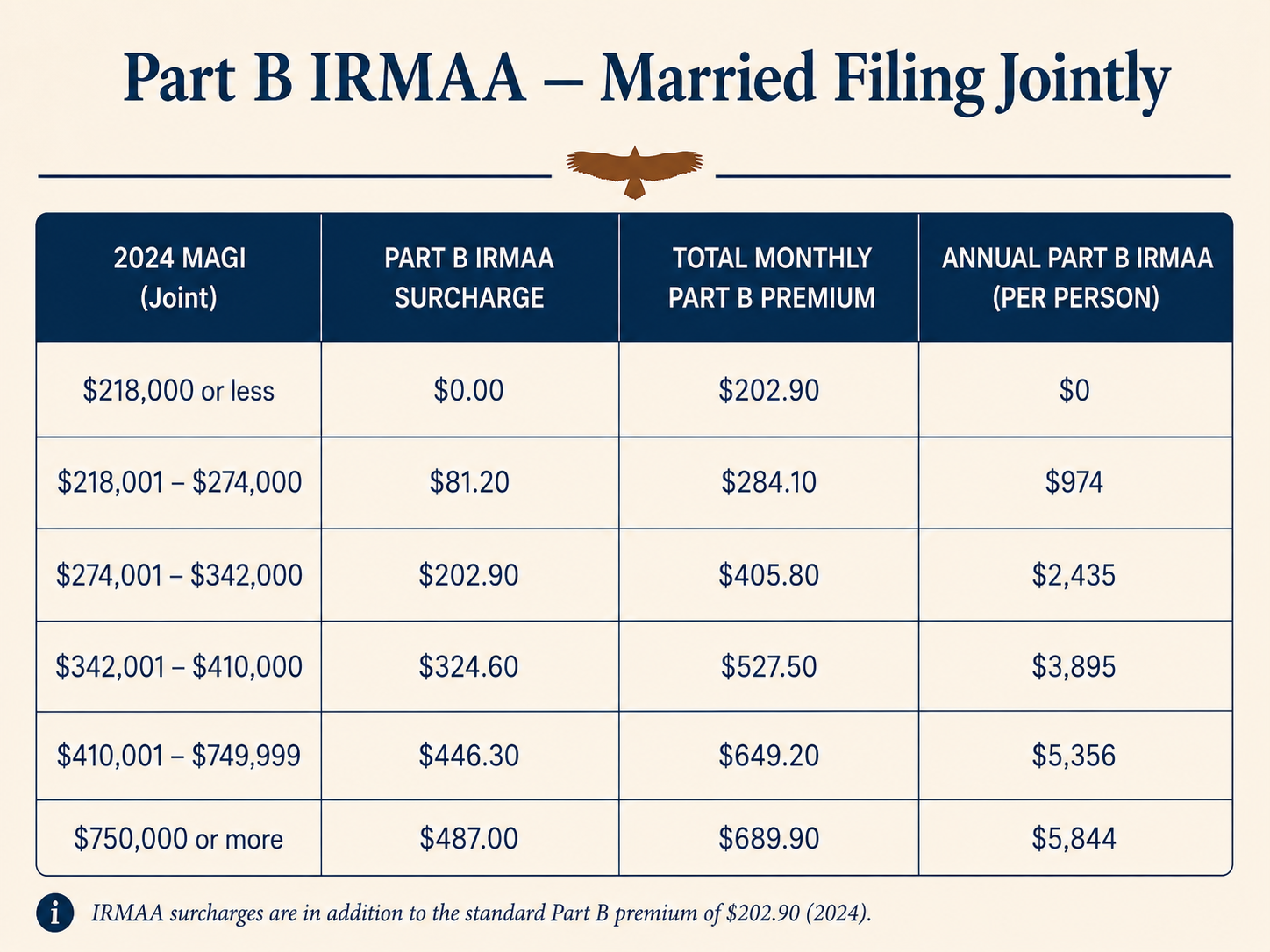

Medicare Part B covers physician services, outpatient care, lab work, durable medical equipment, and most preventive services. The standard 2026 Part B premium is $202.90 per month. IRMAA adds a surcharge on top of that standard amount — ranging from $81.20 to $487.00 per month per person — depending on your income bracket, [according to the official CMS 2026 fact sheet](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles).

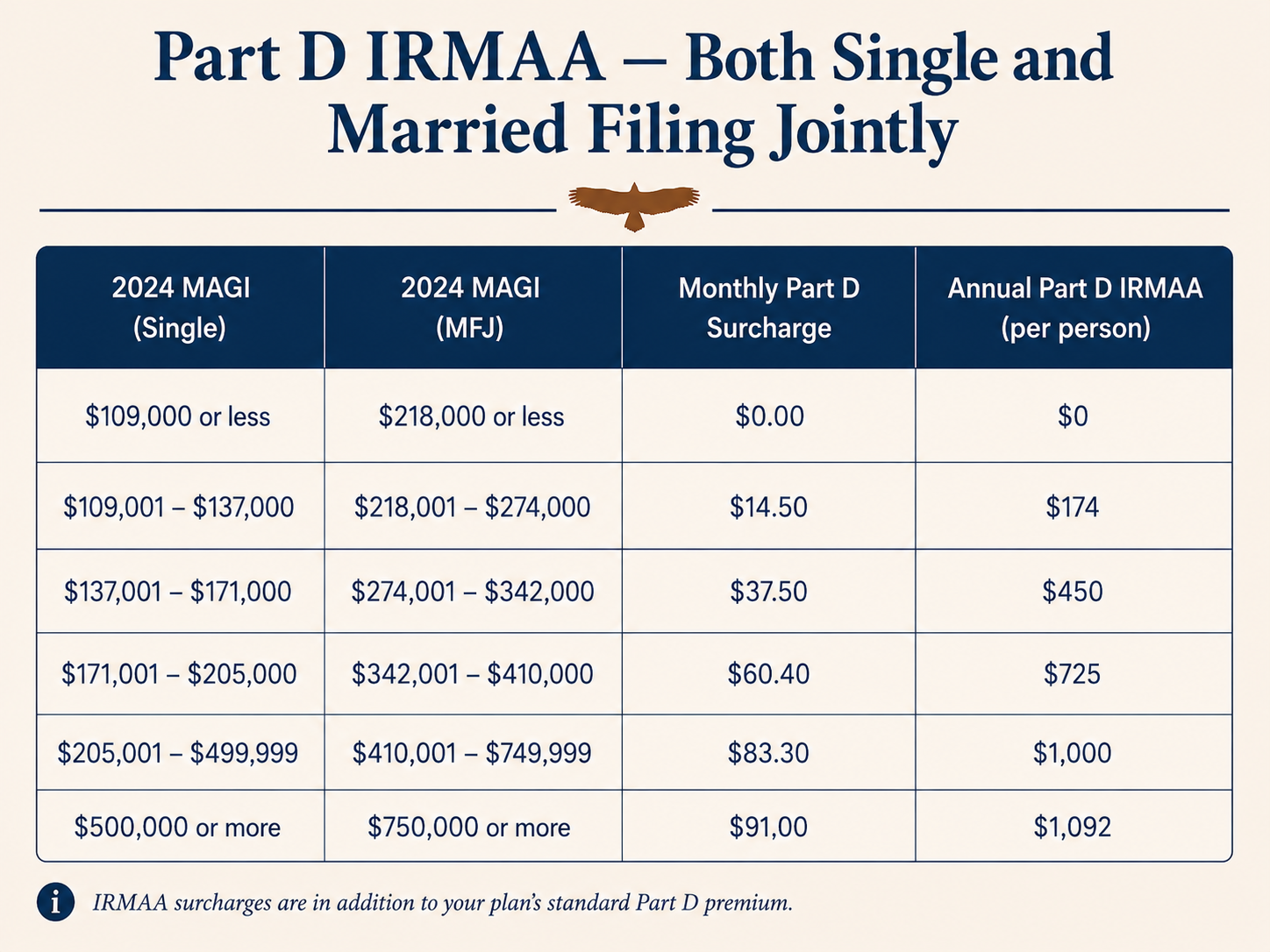

Medicare Part D covers prescription drugs. If you are enrolled in a standalone Part D plan or a Medicare Advantage plan with drug coverage, IRMAA adds a separate monthly surcharge on top of whatever your plan charges. In 2026, Part D surcharges range from $14.50 to $91.00 per month per person. Both surcharges are billed together through your Social Security benefit or as a separate invoice if you are not yet collecting Social Security.

The History — Why IRMAA Exists

IRMAA was created by the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA), which was signed into law in December 2003. The income-related adjustment for Part B premiums took effect in January 2007, [as authorized under Section 1839 of the Social Security Act and Section 811 of the MMA](https://www.ssa.gov/privacy/pia/Medicare%20Modernization%20Act%20(MMA)%20FY07.htm).

The logic: Medicare Part B has historically been subsidized so that premiums cover only about 25% of the actual per-capita cost, with the federal government covering the rest. Congress decided that high-income beneficiaries should shoulder a larger share of that cost. IRMAA initially applied to a narrow slice of high earners, but over time, inflation, rising incomes, and bracket expansions have pulled more retirees into IRMAA territory. Today, roughly 8% of Medicare Part B enrollees pay an IRMAA surcharge — a number that grows each year as more baby boomers retire with substantial retirement assets.

2026 IRMAA Brackets — Full Table

The 2026 IRMAA surcharges are based on your 2024 Modified Adjusted Gross Income (MAGI), as reported on the tax return you filed in 2025. The tables below reflect the official figures released by CMS on November 14, 2025, [available on the CMS newsroom fact sheet](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles). The standard 2026 Part B premium is $202.90/month. IRMAA is added on top of that. Part D surcharges are added on top of your plan's own premium.

*Source: [CMS 2026 Medicare Parts A & B Premiums and Deductibles Fact Sheet](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles), published November 14, 2025.*

**Note:** For married couples filing separately who lived together at any point during the tax year, the brackets compress sharply. Any MAGI above $109,000 triggers the Tier 4 or Tier 5 surcharge — a significant penalty that makes filing status a meaningful planning variable.

How IRMAA Is Calculated — Understanding MAGI

What Counts as MAGI for IRMAA Purposes

For IRMAA, Modified Adjusted Gross Income (MAGI) has a specific, narrow definition. [According to the SSA's Program Operations Manual System (POMS)](https://secure.ssa.gov/poms.nsf/lnx/0601101010), MAGI for IRMAA purposes is:

> AGI (Line 11 of Form 1040) + Tax-Exempt Interest Income (Line 2a of Form 1040)

That's it. Two lines. No other add-backs are used for this calculation — unlike MAGI for Roth IRA eligibility or ACA premium tax credits, which use different formulas entirely.

What this means practically: your municipal bond interest — which is federally tax-exempt and does not appear in your taxable income — still gets counted toward your IRMAA MAGI. Many investors are surprised by this. You can hold a large muni bond portfolio, report zero taxable interest, and still cross an IRMAA bracket because of that Line 2a income. Will IRMA Cost Me Money?

Why MAGI Is Different from Your Taxable Income

Taxable income, the number at the bottom of your return after deductions, can be substantially lower than your MAGI. Your standard deduction or itemized deductions reduce your taxable income but have no effect on your IRMAA MAGI.

A retiree with $150,000 of MAGI might have only $120,000 of taxable income after the standard deduction. They pay income tax based on $120,000 — but their Medicare surcharge is calculated on $150,000. This distinction matters enormously when projecting IRMAA exposure.

Concrete Example: A Couple's MAGI Walk-Through

Here is how MAGI adds up for a hypothetical couple in their first year of retirement:

| Income Source | Taxable? | Counts toward MAGI? | Amount |

|---|---|---|---|

| W-2 wages (partial year) | Yes | Yes | $180,000 |

| Long-term capital gains | Yes | Yes | $20,000 |

| Municipal bond interest | No | Yes | $5,000 |

| Total MAGI | | | $205,000 |

With $205,000 of joint MAGI, this couple falls just at the top of the Tier 2 bracket (MFJ threshold: $274,001 for Tier 3). At $205,000 — assuming they file jointly — they remain just below the first IRMAA threshold of $218,001, so no surcharge applies yet. But if the wife takes a consulting contract adding $15,000, their MAGI hits $220,000, and both partners each owe $81.20 per month in Part B IRMAA — $1,949 combined for the year — on top of the Part D surcharge. One contract tip across one bracket line costs nearly $2,000.

The Two-Year Look-Back Rule

IRMAA is always based on your tax return from two years prior — not your current income. For 2026 Medicare premiums, the SSA uses your 2024 MAGI from the tax return you filed in 2025. [This is established by federal statute as part of the Medicare Modernization Act](https://www.ssa.gov/privacy/pia/Medicare%20Modernization%20Act%20(MMA)%20FY07.htm), and it cannot be overridden except through a qualifying life-event appeal.

Why Your 2024 Income Affects Your 2026 Medicare Premium

The two-year lag exists because the SSA cannot use your current-year income — you haven't filed a return for it yet. So they look backward to the most recent return the IRS has on file. That is almost always the return filed two years before the premium year.

This creates a frustrating mismatch for newly retired people. Someone who earned $350,000 in 2024 — their final year of work — and then retired completely in 2025 will still owe a significant IRMAA surcharge in 2026, even though their retirement income might be $80,000. Their current income has nothing to do with their 2026 bill. Only their 2024 tax return does.

The SSA can use three-year-old data in limited circumstances, but two years is the standard. [The POMS confirms](https://secure.ssa.gov/poms.nsf/lnx/0601101010) that "generally, the information is from two years prior to the year for which the premium is being determined."

What This Means for Planning Windows

For people aged 60–64, the two-year look-back creates a powerful planning window. Every year of income management before you turn 65 has a direct, calculable impact on your Medicare costs in a specific future year.

For people who retire at 63, there is a gap period — sometimes called the gap years — between leaving work and Medicare enrollment at 65. If you retired in 2024 at 63, your 2024 income (with a full year of salary) will set your 2026 Medicare premium. But your 2025 income, mostly from portfolio withdrawals and possibly some Social Security, will determine your 2027 premium. The planning decisions made during those gap years are disproportionately impactful.

The 8 Most Common IRMAA Triggers

1. Large Roth Conversions

Converting traditional IRA or 401(k) funds to a Roth IRA is one of the best long-term tax strategies available — but every dollar converted adds directly to your MAGI for that year. A $100,000 conversion that pushes you across an IRMAA bracket can add $1,949 or more per couple in Medicare costs for a specific future year. The key is converting in the right amount, in the right year. [See the Roth Conversion Pillar for full planning guidance.]

2. Large Capital Gains Events

Selling a business, a rental property, or a concentrated stock position can produce six-figure capital gains in a single year. Even with the favorable long-term rates, those gains are fully included in your MAGI. A couple that realizes $400,000 in gains in one year could land in Tier 4 IRMAA ($446.30/month per person in Part B surcharges), then return to Tier 1 or no IRMAA the following year.

3. RMD Onset at Age 73

Required Minimum Distributions** begin at age 73 under current law. For retirees with large traditional IRAs or 401(k)s, the RMD amount can be substantial — and it counts fully toward MAGI. A $1.5 million IRA generates roughly $56,000 in RMDs in the first year at age 73. Added to Social Security and other income, RMD onset is one of the most common reasons retirees find themselves in unexpected IRMAA brackets.

4. Inherited IRA Distributions

If you inherit a traditional IRA from a non-spouse, you are generally required to deplete the account within 10 years under the SECURE Act rules. Distributions from an inherited IRA count as ordinary income and are fully included in MAGI. Depending on the size of the inherited account, this can push you into a significantly higher IRMAA bracket for multiple consecutive years.

5. Social Security + Roth Conversion Stacking

Each dollar of Roth conversion income can trigger the Social Security taxation torpedo — where additional income causes more of your Social Security benefit to become taxable. The combination is brutal: $50,000 in Roth conversions might add $50,000 to MAGI directly, plus cause an additional $42,500 of previously untaxed Social Security to become included in AGI, effectively increasing your MAGI by nearly $93,000 from a single decision. [See the Social Security Optimization page for a full breakdown.]

6. Net Unrealized Appreciation (NUA) Distributions

If you have company stock inside your employer's retirement plan, the NUA strategy allows you to distribute that stock and pay ordinary income tax only on your cost basis — with the appreciation taxed at preferential long-term capital gains rates. The lump-sum distribution year, however, can significantly spike your MAGI. The strategy often still makes sense, but the IRMAA cost must be factored into the analysis.

7. Surviving Spouse Filing Single

When a spouse dies, the surviving partner typically faces a significant IRMAA exposure in the years after death. In the year of death, they may still file jointly. In subsequent years, they file as single — with brackets that are exactly half those of the married filing jointly thresholds. A surviving spouse with $160,000 of MAGI would owe no IRMAA as a joint filer ($218,000 threshold) but lands in Tier 2 as a single filer ($137,001–$171,000 threshold). This "widow's penalty" is real and quantifiable — and planning for it before the fact is far easier than addressing it after.

8. Large Bonus, Severance, or Business Sale

Significant one-time income events in the years immediately before Medicare enrollment — severance packages, final bonus payments, earnouts from a business sale, or key-man insurance proceeds — can lock in IRMAA surcharges for a specific future year with little ability to mitigate after the fact. The two-year look-back means these events have a delayed but very concrete Medicare cost.

Strategies to Avoid or Minimize IRMAA

Roth Conversion Ladder Planning

Roth conversion ladder is the practice of systematically converting portions of your traditional IRA to a Roth IRA over multiple years — staying within a carefully calculated MAGI limit to avoid IRMAA bracket creep. The sweet spot is converting enough to maximize the long-term tax benefit without crossing an IRMAA threshold. For many clients, this means modeling the exact IRMAA bracket boundaries into the conversion amount each year.

The best window for Roth conversions is typically between retirement and age 73, when MAGI is naturally lower and before RMDs force additional income. Done right, a multi-year Roth conversion strategy reduces future RMDs, reduces future IRMAA exposure, and reduces the taxable estate — three benefits from one coordinated strategy. [See a detailed walk-through on the Roth Conversion Pillar page.]

Tax Bracket Management — "Fill the Bracket"

Rather than converting as much as possible in a given year, disciplined IRMAA planning uses the concept of filling the bracket — converting up to but not past an IRMAA threshold. If your MAGI is projected at $190,000 for a joint filer, you have $27,999 of room before hitting the Tier 3 threshold of $274,001 (if projecting forward to 2027 or 2028). A conversion up to that line captures the tax arbitrage without triggering the next tier's surcharge. The planning requires accurate MAGI projections — not just a look at last year's return.

Qualified Charitable Distributions to Satisfy RMDs

A Qualified Charitable Distribution (QCD) allows people aged 70½ or older to transfer up to $105,000 per person in 2026 directly from a traditional IRA to a qualified charity. The distribution satisfies all or part of your RMD obligation — without the funds ever appearing in your AGI. A $40,000 QCD that satisfies $40,000 of RMD removes $40,000 from your MAGI. For charitably inclined retirees, QCDs are often the single most efficient IRMAA-reduction tool available.

Tax-Loss Harvesting in Taxable Accounts

Tax-loss harvesting — selling positions with unrealized losses to offset capital gains — can reduce the realized gains that flow into your MAGI in a given year. This is particularly useful in years with large planned capital gains events (such as a portfolio rebalancing or a property sale). Systematic loss harvesting throughout the year, rather than just at year-end, tends to produce better results. See the Tax Planning Service Page for more on our approach.

Strategic Withdrawal Sequencing

The order in which you draw from different account types has a direct effect on your MAGI each year. Withdrawals from Roth IRAs are not included in MAGI. Withdrawals from traditional IRAs and 401(k)s are. A retiree who needs $120,000 of spending money might draw $80,000 from a traditional IRA and $40,000 from a Roth — keeping MAGI at $80,000 plus any other income sources — rather than drawing the full $120,000 from the traditional IRA and inflating MAGI unnecessarily. The sequencing decision is re-evaluated each year as income sources and brackets shift.

Bunching Deductions and Donor-Advised Funds

For retirees who itemize, bunching deductions into alternating years can smooth out MAGI variability. A donor-advised fund (DAF) is particularly useful: you contribute a large amount to the DAF in a high-income year (generating a deduction that reduces AGI), then distribute from the DAF to charities over subsequent years at your discretion. This allows you to take a larger deduction in the year you need it most — without being forced to commit to specific charities on that timeline.

Asset Location — Tax-Deferred vs. Taxable vs. Roth

Asset location** refers to the strategic placement of different investment types across account types with different tax treatment. Placing high-yield bonds and REITs in tax-deferred accounts, equities in taxable accounts (for favorable capital gains treatment), and growth assets in Roth accounts can meaningfully reduce the flow of income into your MAGI each year. Over a 20-year retirement, optimized asset location can be worth hundreds of thousands of dollars in after-tax wealth — and significantly reduces IRMAA exposure along the way.

How to Appeal IRMAA Using Form SSA-44

If your income has dropped significantly since the tax year the SSA is using to calculate your IRMAA, you may be able to appeal. The mechanism is Form SSA-44, the Medicare Income-Related Monthly Adjustment Amount Life-Changing Event form, [available directly from the SSA](https://www.ssa.gov/forms/ssa-44.pdf).

The 8 Qualifying Life-Changing Events

The SSA recognizes eight specific events that may qualify you for a redetermination based on more recent income, [as defined in the SSA-44 instructions](https://www.ssa.gov/forms/ssa-44.pdf):

1. Marriage

2. Divorce or annulment

3. Death of a spouse

4. Work stoppage (you or your spouse stopped working)

5. Work reduction (you or your spouse reduced your hours or pay)

6. Loss of income-producing property (due to circumstances beyond your control — natural disaster, fraud, etc.)

7. Loss or reduction of pension income

8. Receipt of an employer settlement payment (severance, wrongful termination payment, or employer closure)

The most commonly used event for pre-retirees and newly retired clients is work stoppage: you retired, your income fell, and the SSA should use more current income to set your premium. The event must have caused a meaningful reduction in MAGI compared to the look-back year being used.

How to File SSA-44

To file, you will need:

- Completed Form SSA-44 (download at ssa.gov or pick up at any Social Security office)

- Evidence of the qualifying event — marriage certificate, divorce decree, death certificate, employer letter confirming retirement date, or equivalent documentation

- Evidence of your reduced MAGI — a signed copy of your most recently filed federal tax return, or a signed estimate of your current-year income if the tax return for that year has not yet been filed

You can submit Form SSA-44 in person at a local Social Security office (sometimes resolved the same day), or by mail to your [local SSA office](https://www.ssa.gov/medicare/lower-irmaa). In-person submission is generally faster. If approved, the IRMAA reduction is typically applied retroactively to the beginning of the year, or to the date of the life-changing event — whichever is later.

Processing time for mailed appeals typically runs 4 to 12 weeks.

When to File vs. When to Wait

File as early in the calendar year as possible if you know your income has dropped significantly. The earlier you file, the sooner any retroactive credit is applied. If your income drop is still in progress (you retired mid-year and the final income numbers aren't yet known), a signed estimate of expected MAGI is acceptable at the time of filing — you will need to provide the actual return once it is filed.

Do not wait until year-end if you retired in January. You may be overpaying your IRMAA surcharge for 11 months unnecessarily.

IRMAA Planning Timeline by Age

Ages 60–64: Pre-Medicare Planning Window — Most Powerful

This is the highest-leverage IRMAA planning window you have. Every income decision made from age 60 to 64 has a direct, calculable effect on your Medicare premiums at age 65, 66, or 67. Specifically:

- Your age-63 income will determine your age-65 Medicare premium

- Your age-64 income will determine your age-66 Medicare premium

Key priorities for this window: begin modeling your post-retirement MAGI, identify which years are optimal for Roth conversions, consider accelerating or deferring any large capital gains events, and set a QCD strategy if you are already 70½. Many clients who manage this window well arrive at Medicare enrollment in Tier 1 or with no IRMAA at all — saving thousands per year in perpetuity.

Subscribe to the Wealth Hawk Report to receive our annual IRMAA planning checklist each October, when the new brackets are released.

Ages 65–72: Medicare Enrollment + Roth Conversion Opportunity

Once you enroll in Medicare, IRMAA is live — but the planning doesn't stop. The years between 65 and the start of RMDs at 73 are an important conversion window. Your MAGI is often lower in these years (no longer earning a salary, not yet taking RMDs), making it an ideal time to execute a Roth conversion ladder at controlled MAGI levels.

Also during this period: watch for life events that qualify you for a Form SSA-44 appeal, review your IRMAA tier each fall when the Social Security Administration sends your premium notice, and coordinate with any Social Security claiming decisions — because the timing of Social Security benefits affects MAGI significantly. [See the Social Security Optimization page for claiming strategy guidance.]

Ages 73+: RMD Era — Defensive Planning

Once RMDs begin, the planning shifts from offensive (reducing MAGI through conversions) to defensive (managing the income that RMDs force into your return). Key strategies in this phase:

- QCDs to offset RMDs without MAGI impact

- Charitable remainder trusts for large asset sales

- Annual IRMAA tier monitoring each October-November when new brackets are announced

- Surviving spouse planning — proactively model the bracket impact of the surviving partner filing single

Roth conversions may still make sense in the RMD era if your health suggests significant longevity or if your estate planning goals favor building Roth assets for heirs. This requires case-by-case analysis.

Common IRMAA Mistakes to Avoid

1. Assuming your accountant is managing IRMAA. Most tax preparers focus on filing your return accurately and minimizing the current year's tax bill. IRMAA planning requires projecting income two years forward and coordinating withdrawals, conversions, and distributions — it is a financial planning function, not a tax preparation function.

2. Ignoring tax-exempt interest. Muni bond income, even though it reduces your federal tax liability, counts toward your IRMAA MAGI. Holding a large municipal bond allocation can push you into a surcharge bracket you wouldn't otherwise reach.

3. Treating IRMAA thresholds as soft targets. IRMAA is a cliff, not a slope. If your MAGI exceeds a threshold by $1, you pay the full surcharge for that bracket for the entire year. The difference between $218,000 and $218,001 of joint MAGI in 2026 is $1,949 in combined Medicare costs.

4. Missing the Form SSA-44 window after retirement. Many people retire and simply accept the high IRMAA surcharge for two years, not knowing they can appeal immediately based on the retirement as a qualifying life event.

5. Failing to plan for the surviving spouse bracket compression. The death of a spouse doesn't reduce Medicare costs — it often increases them significantly, because the survivor shifts from married filing jointly thresholds to single thresholds that are half as wide. This is a predictable risk that can be partially addressed with proactive Roth conversion and income positioning while both spouses are living.

6. Running Roth conversions without MAGI guardrails. A Roth conversion that feels like a good tax-planning move can inadvertently add $1,000–$5,000 per couple in Medicare costs if it crosses an IRMAA bracket. Conversions need to be sized against both the federal income tax brackets and the IRMAA brackets simultaneously.

How a Fee-Only Fiduciary Helps with IRMAA Planning

IRMAA planning sits at the intersection of tax strategy, Social Security timing, investment sequencing, and Medicare enrollment. Getting it right requires someone who understands all four — and who has no financial incentive to recommend one approach over another.

At Sentient Financial, Patrick Thompson works with pre-retirees and retirees who have $1 million or more in investable assets and want a clear, coordinated plan rather than piecemeal advice. The IRMAA planning process follows four steps:

1. Discovery Call — Understanding your full income picture: salary, Social Security timing, IRA and brokerage balances, pensions, rental income, and any anticipated one-time events (business sale, inheritance, etc.)

2. MAGI Projection Model — Building a multi-year forward projection of your expected MAGI for each year from now through your mid-80s, identifying which years carry IRMAA risk and which offer conversion opportunities

3. Roth Conversion Analysis — Sizing conversions against both the federal income tax brackets and the IRMAA bracket boundaries to find the optimal amount for each year

4. Annual Review — Revisiting the model each year, especially each October when new IRMAA brackets are announced, to adjust as needed

As a fee-only fiduciary registered in California, Sentient Financial charges for advice — not for products. There are no commissions, no conflicts of interest, and no reason to recommend anything other than what is genuinely in your best interest.

See the Tax Planning Service Page to learn more about how we approach MAGI management as part of a comprehensive retirement income plan.

Frequently Asked Questions

What is IRMAA?

IRMAA stands for Income-Related Monthly Adjustment Amount. It is a surcharge added to your Medicare Part B and Part D premiums if your income exceeds certain thresholds. The SSA determines your IRMAA using your MAGI from two years prior. It is not a penalty — it is a means-tested pricing structure built into Medicare law since 2007.

What are the 2026 IRMAA brackets?

For 2026, IRMAA surcharges begin when your 2024 MAGI exceeds $109,000 (single) or $218,000 (married filing jointly). The Part B surcharge ranges from $81.20 to $487.00 per month per person; the Part D surcharge ranges from $14.50 to $91.00 per month per person. Full bracket tables are provided above, sourced from the [official CMS fact sheet](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles).

How does the IRMAA two-year look-back work?

The SSA uses your tax return from two years prior to set your Medicare premium. Your 2026 IRMAA is based on your 2024 MAGI — the most recent return the IRS has on file when 2026 begins. If you retired in 2025 and your income dropped significantly, you can appeal using Form SSA-44 rather than waiting two years for the surcharge to fall on its own.

How can I avoid IRMAA?

The most effective strategies are Roth conversion laddering timed to stay below IRMAA thresholds, using Qualified Charitable Distributions to satisfy RMDs without increasing MAGI, strategic withdrawal sequencing (drawing from Roth accounts to supplement traditional IRA withdrawals), and tax-loss harvesting to offset capital gains. No single strategy works in isolation; the best results come from an integrated multi-year plan.

Can I appeal my IRMAA determination?

Yes. If you have experienced a qualifying life-changing event that has reduced your income — retirement, reduced work hours, divorce, death of a spouse, loss of a pension, or an employer settlement — you can request a redetermination using Form SSA-44. The SSA will use your more recent income to determine your surcharge rather than the standard look-back year.

What is Form SSA-44?

[Form SSA-44](https://www.ssa.gov/forms/ssa-44.pdf) is the Medicare Income-Related Monthly Adjustment Amount Life-Changing Event form. You file it with the Social Security Administration to request that they use more recent income — rather than the standard two-year look-back — to calculate your IRMAA. It requires documentation of both the qualifying life event and your estimated or actual current income.

Do Roth conversions cause IRMAA?

Yes, they can. Every dollar converted from a traditional IRA to a Roth IRA is included in your gross income for that year and adds directly to your MAGI. A large Roth conversion can push you across an IRMAA bracket, resulting in a two-year IRMAA surcharge on the Medicare premiums you pay in the year that is two years after the conversion. Careful bracket management — converting up to but not past IRMAA thresholds — is essential.

Are capital gains counted for IRMAA?

Yes. Both short-term and long-term realized capital gains are included in your AGI and therefore in your MAGI for IRMAA purposes. This includes gains from selling stocks, mutual funds, real estate, or a business. Unrealized gains do not affect MAGI — only gains that are realized (sold) in the tax year count.

Is IRMAA permanent or does it reset each year?

IRMAA resets every year. Each year, the SSA reviews your most recent available tax return and determines whether a surcharge applies for the coming year. If your income drops — through retirement, completed Roth conversions, or any other reason — your IRMAA surcharge falls with it in the subsequent determination cycle. It is not a permanent condition.

Does Social Security income count for IRMAA?

The taxable portion of your Social Security benefit is included in your AGI and therefore affects your MAGI. For most high-income retirees, up to 85% of Social Security benefits are taxable. The non-taxable portion (up to 15%) does not count toward MAGI. This makes Social Security timing a meaningful IRMAA planning variable, particularly in years when large Roth conversions or capital gains events are also planned.

What’s Your Next Step?

You've learned how IRMAA fits into retirement.

Now see how it fits into your retirement.

Take the Retirement Readiness Checkpoint

In about 2-minutes, you'll discover how well your retirement income, taxes, Medicare, Social Security, and investment decisions work together—and where there may be opportunities to improve coordination.

Want to keep learning?

Should I Convert to Roth This Year?

Learn how Roth conversions may reduce future taxes and help manage Medicare premiums.

Should I Retire This Year or Next?

See how the timing of your retirement can affect taxes, Medicare, Social Security, and your long-term income plan.

How Much Retirement Income Can My Portfolio Support?

Estimate how much sustainable income your investments may be able to generate.

Retirement Transition Series

Watch short educational videos covering the biggest financial decisions before and during retirement.

Sentient Financial, LLC is a state-registered investment adviser in California. This information is for educational purposes only and does not constitute investment, tax, or legal advice. Nothing here should be taken as a recommendation to buy or sell securities or to implement a specific strategy. IRMAA thresholds and Medicare premiums change annually — figures shown are for the 2026 plan year and should be verified against the official CMS announcement at [cms.gov](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles). Consult a qualified tax professional before implementing any strategy. Past performance does not guarantee future results.