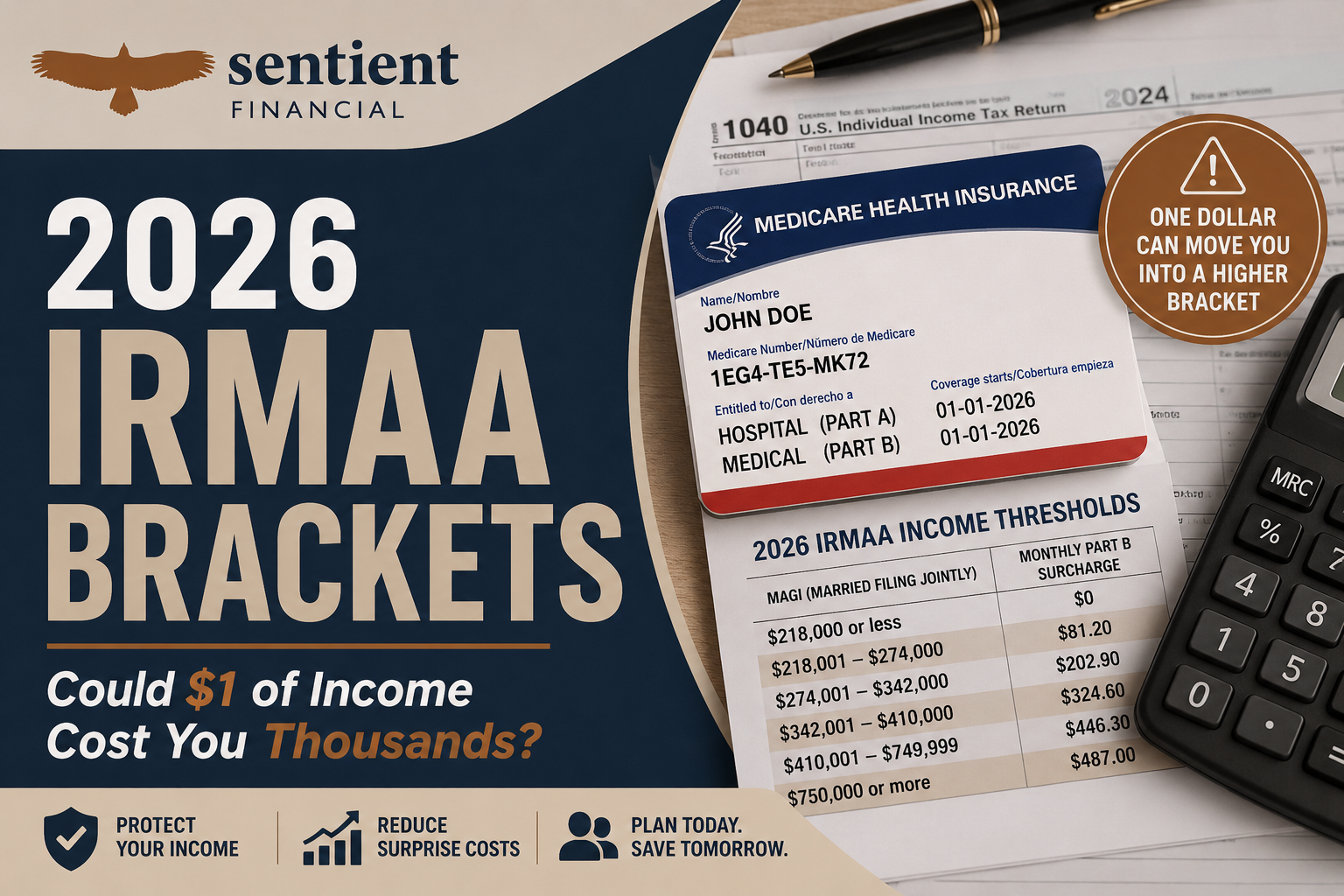

IRMAA Brackets 2026: How Much Will You Pay for Medicare?

Here is a number that should get your attention: $13,872. That is the additional amount a married couple in the highest 2026 IRMAA bracket pays for Medicare on top of what their lower-income neighbor pays — for exactly the same coverage. And the income that triggered it? Their 2024 tax return, filed two years before Medicare even sent a bill. If you are 62 or older, the decisions you make about income this year directly determine what you will pay for Medicare in 2026. This post lays out every bracket, every dollar, and the strategies that can keep more money in your pocket.

What Are the 2026 IRMAA Brackets?

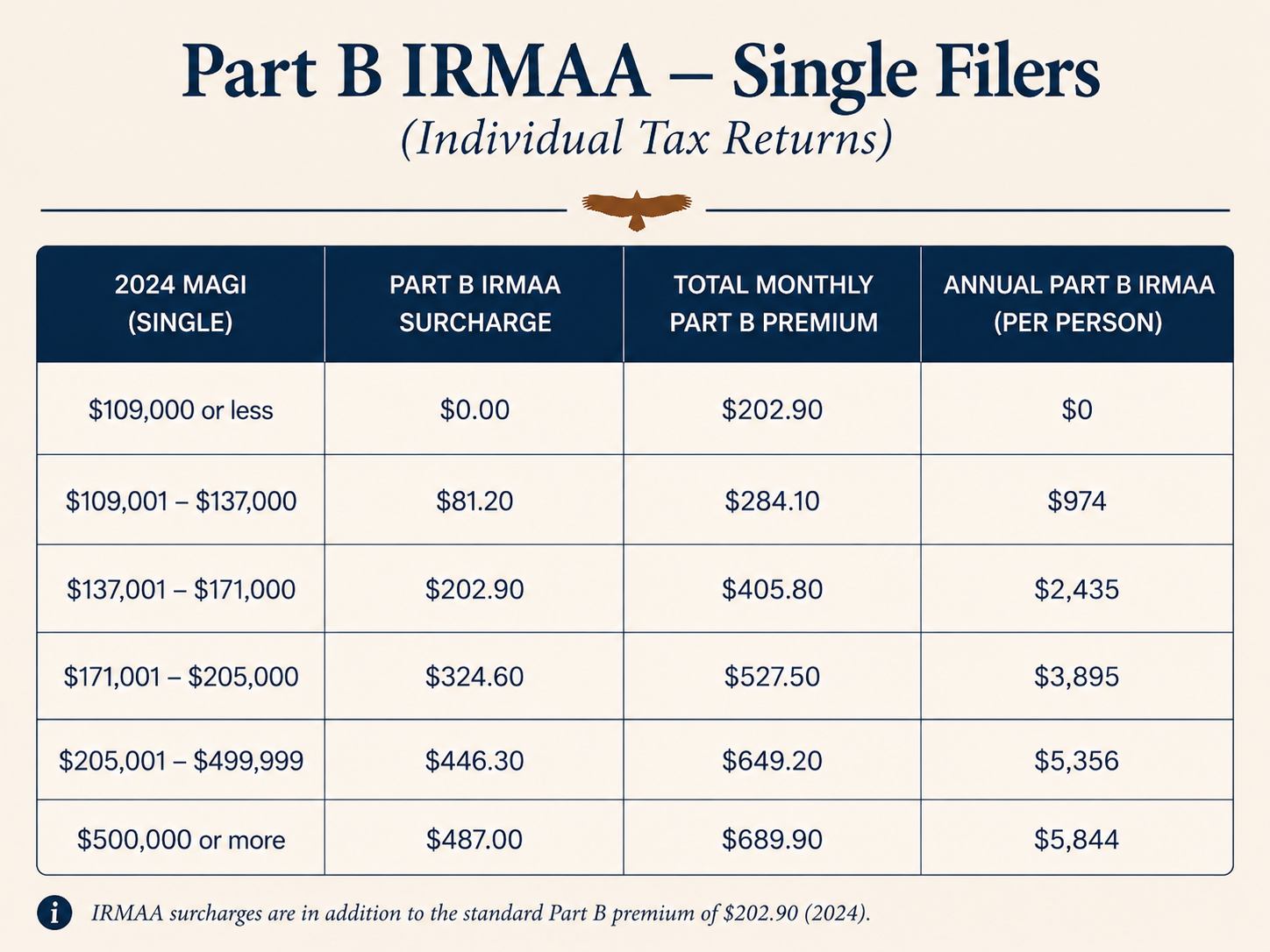

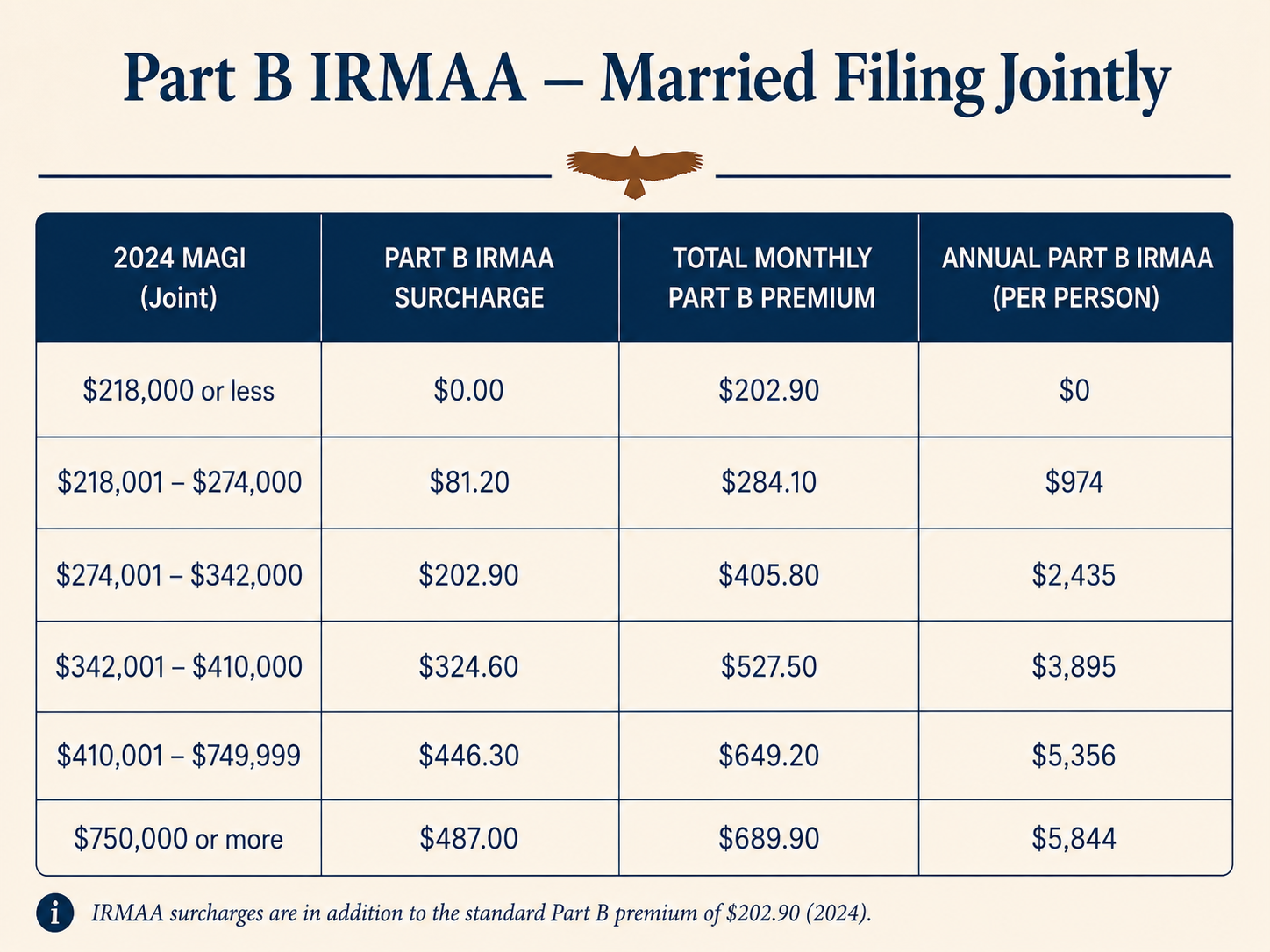

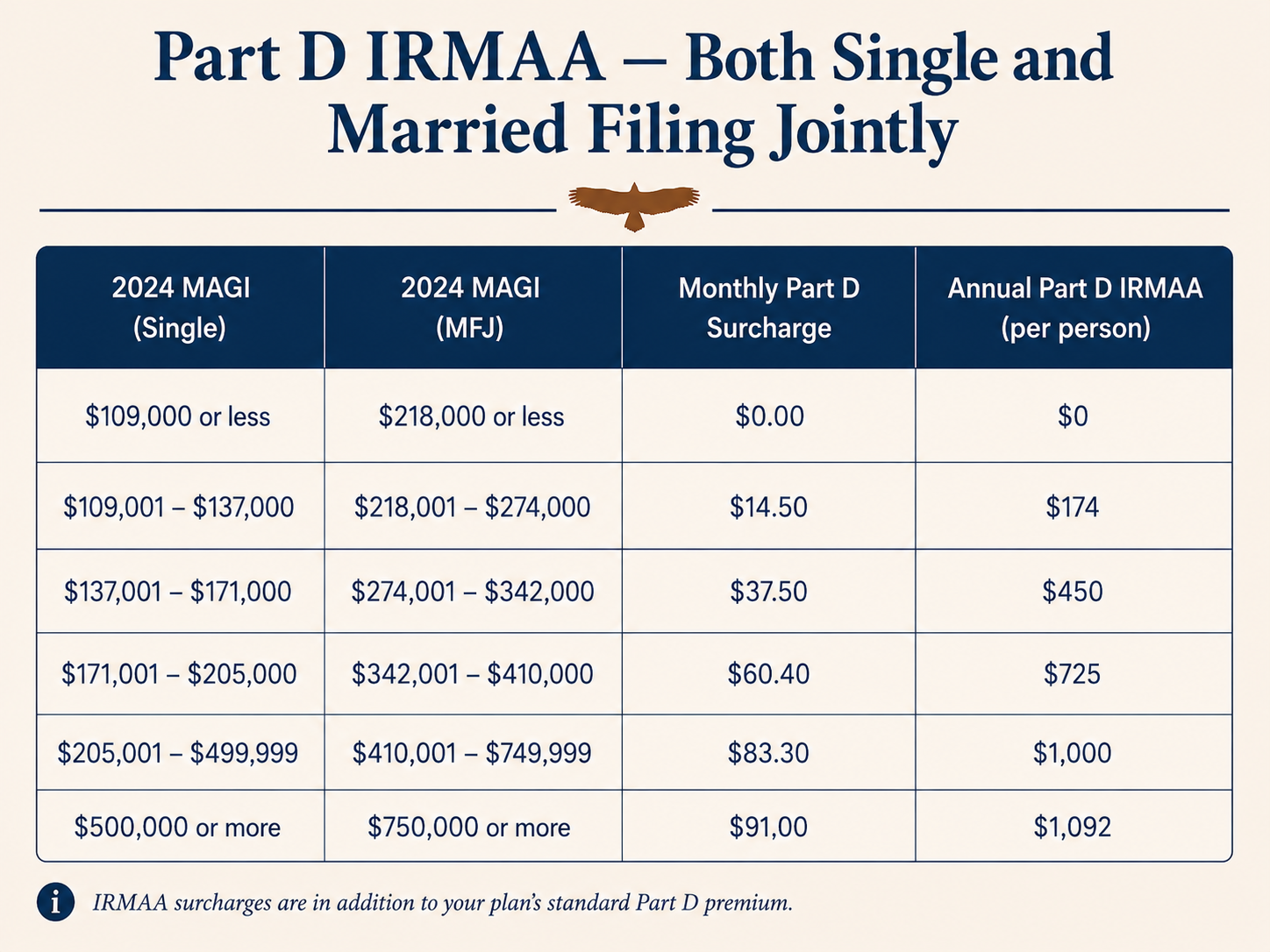

The 2026 IRMAA brackets are the income thresholds that determine how much you pay in Medicare Part B and Part D surcharges. Your position within these brackets is set by your 2024 Modified Adjusted Gross Income (MAGI), which Social Security pulls from your IRS tax records. There are five surcharge tiers, each progressively more expensive than the last.

Source for all figures in this post: Centers for Medicare & Medicaid Services, 2026 Medicare Parts A & B Premiums and Deductibles

The Complete 2026 IRMAA Bracket Tables

Part B Premiums by Income Tier

Part D Surcharges by Income Tier

Note for married filing separately: If you lived with your spouse at any point during the tax year, the brackets are much harsher. IRMAA jumps immediately to $446.30 per month in Part B surcharges if your MAGI exceeds $109,000, with no intermediate tiers.

Special Rule for Married Filing Separately

2024 MAGI — Married Filing Separately (lived together) - Monthly Part B Premium / Monthly Part D Surcharge

$109,000 or less - $202.90 / $0

$109,001 – $390,999 - $649.20 / $83.30

$391,000 or more - $689.90 / $91.00

This is one of the most penalizing aspects of the IRMAA rules. Couples who choose to file separately hoping to reduce individual incomes get almost no benefit from the intermediate tiers — the surcharge jumps from zero directly to the fourth tier.

What This Costs in Real Annual Dollars

Looking at monthly surcharges can obscure the true cost. Here is what IRMAA actually costs per year, per person, for Part B and Part D combined in 2026:

Tier / Single MAGI Range / Annual Part B + Part D IRMAA Surcharge (Per Person ) / Per Couple

No IRMAA / ≤ $109,000 / $0 / $0

Tier 1 / $109,001 – $137,000$ / 1,148 / $2,297

Tier 2 / $137,001 – $171,000 / $2,886 / $5,772

Tier 3 / $171,001 – $205,000 / $4,620 / $9,240

Tier 4 / $205,001 – $499,999 / $6,355 / $12,710

Tier 5 / $500,000 or more / $6,936 / $13,872

A married couple who earned $420,000 in 2024 sits in Tier 4. They pay $12,710 more per year in Medicare premiums than a couple earning $215,000 — with identical benefits. Over a 20-year retirement, that is $254,200 in extra premiums at today's rates, before any future increases.

How the Brackets Are Set Each Year

The 2026 brackets are not plucked from thin air. The Centers for Medicare & Medicaid Services (CMS) announces them each November, tied to the previous year's Part B premium costs and adjustments for healthcare inflation. Most of the bracket thresholds — those below the top tier — are adjusted annually for general inflation. The top brackets ($500,000 for individuals, $750,000 for joint filers) are fixed by statute.

For 2026, the income thresholds increased by approximately 3% from 2025 levels, while the actual surcharge dollar amounts increased about 9%, reflecting rising healthcare costs. [Learn how the two-year look-back determines which year's brackets apply to you].

The Bracket Cliff Effect

IRMAA is not a gradual, proportional surcharge. It is a tiered system with sharp cliffs. If your 2024 MAGI is $136,999, your monthly Part B premium is $284.10. If it is $137,001 — just $2 more — your monthly premium jumps to $405.80. That is an extra $1,464 per year triggered by $2 of additional income.

This cliff effect is why bracket management is so important. Here is a scenario that illustrates what is at stake:

The Roth Conversion Cliff

Robert and Sandra are married, both 67, and both on Medicare. Their 2024 MAGI consists of:

Social Security: $58,000 (combined)

Pension: $90,000

Dividends and interest: $45,000

Running total: $193,000

They are safely below the $218,000 threshold and pay the standard Part B premium with no IRMAA. Their advisor recommends a Roth conversion to reduce future RMDs. If they convert $80,000, their MAGI rises to $273,000 — just $1,000 below the $274,000 Tier 2 cutoff. They stay in Tier 1, paying $81.20 per person per month in surcharges.

But if they convert $82,000, their MAGI becomes $275,000 — $1,001 above the $274,000 boundary. They fall into Tier 2 at $202.90 per month per person. The extra $2,000 of Roth conversion triggered an extra $2,904 per year in Medicare premiums. The numbers must be run with precision.

Why Your 2025 Income Decisions Matter for 2027

The two-year look-back means that planning for IRMAA is always working two years ahead. If it is 2026, Social Security is reading your 2024 tax return. But 2025 income decisions you made last year will set your 2027 IRMAA.

This has critical implications for:

Roth conversions: The income you convert in 2025 determines whether you face IRMAA in 2027.

Capital gains realizations: Selling appreciated assets in 2025 affects 2027 premiums.

RMD timing: If you turned 73 in 2025 and took your first RMD in April 2026 (as the rules allow for the first year), that delayed distribution still counts as 2026 income for IRMAA purposes — and hits your 2028 premiums.

[Read our full explanation of the IRMAA two-year look-back rule].

Who Gets Caught Off Guard by IRMAA

The people most likely to be surprised by IRMAA are:

Newly retired executives or professionals. Your last working year had high W-2 income. Medicare begins, and the premiums are based on that high-earning year — not on your first year of retirement income.

Business owners who sold their company. A business sale often generates a large one-time capital gain that puts you in a high IRMAA tier for two years.

Couples doing large Roth conversions. Well-intentioned tax planning can accidentally push income over an IRMAA threshold.

Retirees with large traditional IRA balances. When RMDs begin at 73, they can push MAGI well above the initial IRMAA threshold, even in years where no other income change occurred.

Strategies to Stay Below Key IRMAA Thresholds

The $109,000 (individual) and $218,000 (married) thresholds are the most important lines to monitor. But managing within any bracket boundary is worth the effort given the cliff effect. Strategies that can help include:

Roth conversion management: Converting just enough to stay within your current IRMAA tier — no more.

Qualified Charitable Distributions (QCDs): Available at 70½ and older, QCDs move IRA money to charity without adding to MAGI. In 2026, you can direct up to $108,000 per person directly from your IRA to qualified charities — satisfying your RMD without raising your income.

Tax-loss harvesting: Realized capital losses offset gains and can keep your MAGI below a bracket boundary.

Municipal bond interest: This is a trap, not a solution. Municipal bond interest counts toward IRMAA MAGI even though it is not taxed. Shifting from munis to other tax-advantaged investments may help.

HSA contributions before Medicare: If you are still working past 65 and have a high-deductible health plan, HSA contributions reduce your MAGI dollar-for-dollar. Once you enroll in Medicare, you can no longer contribute to an HSA, but distributions are tax-free for medical expenses and do not affect MAGI.

If you have already crossed a threshold due to a one-time event — a business sale, an inheritance, or your last year of high income — an IRMAA appeal using Form SSA-44 may allow you to use a more recent year's income instead.

Frequently Asked Questions About the 2026 IRMAA Brackets

When did CMS announce the 2026 IRMAA brackets? CMS announced the 2026 IRMAA brackets in November 2025 as part of the annual Medicare Parts A & B Premiums and Deductibles announcement. The effective date for 2026 premiums is January 1, 2026.

What income is used to determine my 2026 IRMAA bracket? Your 2024 MAGI — Modified Adjusted Gross Income plus tax-exempt interest income — as reported on your 2024 federal tax return. The Social Security Administration uses this figure to set your 2026 premiums.

Do IRMAA brackets apply to Medicare Advantage (Part C) plans? Part B IRMAA applies to your underlying Part B premium regardless of whether you are in Original Medicare or a Medicare Advantage plan. However, the plan-level premium that you pay to a Medicare Advantage insurer is separate and is not directly affected by IRMAA.

If my income dropped significantly in 2025, can I get lower premiums in 2026? Possibly. If the income drop was due to a qualifying life-changing event (retirement, divorce, death of a spouse, loss of income-producing property), you can file Form SSA-44 to ask Social Security to use a more recent year's income. A general market loss or investment decline does not qualify as a life-changing event.

Are IRMAA surcharges tax-deductible? IRMAA surcharges are Medicare premiums, and Medicare premiums are generally tax-deductible as medical expenses if you itemize deductions and your total medical expenses exceed 7.5% of your AGI. For self-employed individuals, Part B premiums (including IRMAA surcharges) may be deductible as self-employed health insurance. Consult a tax professional for your specific situation.

Are the 2027 IRMAA brackets already known? Not yet. CMS typically announces the following year's brackets in November. The 2027 brackets will be announced in November 2026, based on 2025 MAGI.

Let's Make Sure You Are in the Right Bracket — Not a Higher One

IRMAA bracket management is a precision exercise, not a rough estimate. A $2,000 income decision in the wrong direction can cost $2,900 per year in Medicare premiums. If you are within a few years of retirement or already on Medicare, it is worth a careful look at your projected income versus the bracket thresholds — before you make irreversible moves like a large Roth conversion or a significant asset sale. I offer a complimentary 20-minute Retirement Fit Call specifically to help pre-retirees and recent retirees understand what they are up against.

Visit the Complete Guide to IRMAA Planning

Sentient Financial, LLC is a state-registered investment adviser in California. This information is for educational purposes only and does not constitute investment, tax, or legal advice. Nothing here should be taken as a recommendation to buy or sell securities or to implement a specific strategy. Past performance does not guarantee future results. All IRMAA figures are for the 2026 benefit year as published by the Centers for Medicare & Medicaid Services and are based on 2024 MAGI.